With Human Input Declining What Needs to Be Done to Continue Gdp Growth Rmi

This article was written by Petri Mäki-Fränti, Arto Kokkinen (NAOF) and Meri Obstbaum; it is based on a BoF Economics Review article published on 16 December 2021.

Decline in working-age population and low productivity weakening outlook for growth

Decision-making in economic policy relies not only on short-term economic forecasts, but also on forecasts of long-term growth prospects. In projections published by the Bank of Finland in the 2010s, economic growth in Finland was predicted to remain at around 1.5% over the following few decades, which is a considerably slower rate of growth than what had been the norm prior to that decade.See, for example, Obstbaum, M. – Mäki-Fränti, P. (2018) Finland's long-term growth prospects moderate – Bank of Finland Bulletin (bofbulletin.fi) 6 July 2018. The prospects for growth in Finland in the next few decades presented in this article are poorer than what was anticipated on the basis of previous long-term forecasts made by the Bank of Finland.

The outlook for economic growth in Finland is weakened by a decline in the working-age population as the population ages and by the poor trend in labour productivity. Productivity growth will slow particularly due to a lack of fixed capital investment and the poorer prospects for human capital, measuring the volume of human capital in terms of qualifications valued by the volume of expenditure on education services per student. In addition, the demand for age-related health and care services, which display weak productivity growth, continues to increase. These services will in the future account for a larger number of people in the labour force than ever before. Slow productivity and economic growth, in a situation where the need for age-related public services is at the same time growing, will put pressure on the sustainability of the public finances.

This article sets out the Bank of Finland's new long-term forecast for the Finnish economy for the period 2020–2070. The main difference between this new forecast and its predecessors is that it emphasises the importance of human capital as a source of economic growth. In previous studies and forecasts for growth in the Finnish economy, economic growth would typically be explained within the framework of growth accounting with reference to the rate of growth of labour input, the fixed capital stock and total factor productivity. Here, we show that labour productivity growth in Finland in past decades can be explained simply in terms of investment in fixed and human capital. The long-term growth forecast can thus be based on projections for the growth in fixed and human capital in Finland in the period 2020–2070. In this article, investment in human capital accumulation is measured for Finland in terms of the volume of public expenditure on education services per student.

The forecast is a projection where the assumption is that the growth in production factors will continue broadly to reflect earlier trends. Technological progress, which, in growth contribution analysis based on the neoclassical production function, is thought to result in an increase in total factor productivity, is included in fixed capital in the economic statistics as they are currently. Technological progress thus comes about in an empirical application of the forecasting model through renewal of the capital stock. The advantage in such a case is that there is no need to explain production growth by relying on assumptions about the growth rate for total factor productivity.

Bank of Finland's new long-term forecasting framework

The prospects for long-term economic growth in Finland, too, have mostly been assessed in the context of growth accounting, which is based on neoclassical growth theory. According to that, labour productivity cannot be boosted indefinitely merely by increasing the capital stock per employee, because, with the growth in capital, its impact on increased labour productivity declines and, in the end, fades away. The growth contribution analysis with reference to these models shows that the long-term rate of growth of productivity and GDP depend mainly on the trend in total factor productivity. Put simply, the growth in total factor productivity may be regarded as something that represents general technological progress, which, in the model, is assumed to arise externally. Increased total factor productivity, therefore, does not depend on, for example, levels of education among the population, innovation policy or comparable factors, which can be influenced by the choices made by consumers and companies and those made in the context of economic policy.

Unlike before, the Bank of Finland's new long-term forecasting model is based on endogenous growth theory. The trend in labour productivity is explained, not by total factor productivity, but by the increase in human capital in the economy and in the fixed capital stock, which is also influenced by technological progress in capital goods, as suggested by the statistics. Fixed capital now also includes investment in research and development (R&D), databases, computer software, R&D outputs that support production and other intellectual property products.

Human capital in the model is interpreted as the knowledge and skills of the working-age population that are the result of education and the gaining of qualifications. It is thus possible to measure human capital growth in terms of the qualifications gained by the working-age population, weighted by the volume of education services used for acquiring those qualifications. The entire human input in economic production is reflected in the number of hours worked by a trained labour force.

Technological progress in the model is explained by the regeneration of fixed capital. Although the new forecasting model does not contain a separate account of technological progress, it is important to realise that this is included in the technological advancement of fixed capital products in the updated system of national accounts 2008, which was implemented in the macroeconomic data of the EU countries in 2014.Research and development were defined and recorded in the system of national accounts prior to 2014 in the category intermediate goods and services, which may have also affected the way in which R&D was treated in growth theory models. New production technologies emerge and spread from company to company as existing means of production are replaced by new generation solutions that are more productive than before. Technological progress in an economy therefore actually depends on intangible ideas resulting in the technological advancement of capital products and the volume of capital stock. Technological progress also requires human capital. The innovation and efficient adoption of new technologies is not possible without the knowledge and skills of a professional labour force, constantly updated as they need to be.

A distinct advantage of the new forecasting model, compared with previous models, is that it is possible to explain the growth in labour productivity solely in terms of investment in human and fixed capital. Unlike in conventional models based on neoclassical growth theory, economic growth no longer needs to be explained with reliance on externally determined factors – such as total factor productivity – which are independent of the choices made in the context of economic policy.

As with the Bank of Finland's earlier long-term forecasts, in the new framework for growth, the economy is divided into three parts: public production, manufacturing and private non-manufacturing activities. This division makes it possible to consider the differences in productivity growth in private and public production and among the different industrial classes. In this way it is also possible to examine how the ageing population is impacting the labour supply and labour productivity in private and public production. Finally, production levels calculated for sections of the economy are compiled to give a picture of production for the economy as a whole.

Human capital growth an explanatory factor for economic growth in Finland

The role of human capital as a factor in economic growth has been stressed in studies of economic growth conducted since the 1980s. It has been suggested that human capital acts directly as a factor of production, boosts the efficiency of labour input, or enables technological progress and its adoption. In earlier empirical growth studies, it is the level of education of the working-age population, measured by the number of years spent in education on average, that has frequently been the variable used for the volume of human capital. Although the notion of a link between education levels and human capital is justified in terms of economic theory, the connection in empirical studies between levels of education and economic growth measured in this way has been found to be uncertain.

In this article, the trend in the quality of human capital is examined, not only with reference to how long on average people have been studying, but also in terms of the accumulation of education services used to gain qualifications. As is implied, this is measured cumulatively based on the volume of education expenditure incurred for each qualification. The cumulative education expenditure volume for the education services used to gain the qualifications has been compiled using the method of calculation based on national accounts data developed by Kokkinen (2012).Investment in human capital is in this case compiled and accrued to human capital stock using the similar compilation strategy and perpetual inventory method (PIM) as with fixed capital in the same national accounts framework.The estimate of growth in human capital for the period 1934–2000 is based on the Kokkinen (2012) study. The data for these years were combined with those for the period 2000–2019, which are based on a similar method of calculation, and on more detailed statistics on education. For the period 2000–2019, the new figures for education were available from Statistics Finland. These provided the annual figures for students and qualifications gained by educational level for each cohort of students aged 16 and over. The annual education expenditure volumes for the period 2000–2019 could then be allocated separately for each cohort. The data on education expenditure volumes were based on national accounts figures. In the calculations, the volume of expenditure on education services was allocated to student categories based on educational level (in Finland: compulsory basic education (comprehensive school), upper secondary education and higher education). The allocation was carried out with reference to the number of students at each educational level and the average education expenditure volume per student, which were calculated based on historical data. Finally, the cumulative volume of education expenditure used in basic education was added to the volume of expenditure on post-comprehensive school qualifications.The periods of study, especially for graduating at the level of tertiary education, are long, and knowledge and skills are acquired only gradually. The years needed to gain qualifications are taken into account here in such a way that the volume of education expenditure accumulating during the years of study increases the human capital stock of the economy only at the point when students have gained their highest qualification, stopped studying and entered the labour market. The volume of human capital in the Finnish economy compiled in this way does much to explain economic growth in the country in conjunction with fixed capital in the period 1934–2019.

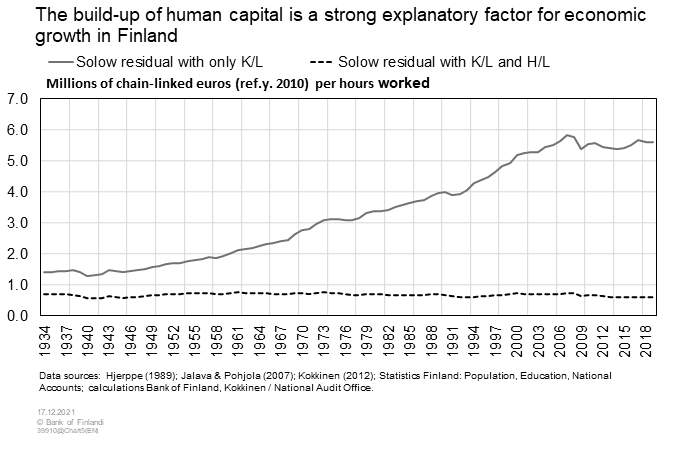

Chart 1 shows the residuals for models where GDP per hours worked is explained, either solely by fixed capital per hours worked, or alternatively, by fixed and human capital per hours worked. That part of production growth that is not explained by the growth in these production factors may be interpreted as the rate of total factor productivity growth. It is to be noted that, in the second model, total factor productivity as an explanatory factor for labour productivity growth is substantially less significant.

Human capital in danger of declining in Finland

The human capital stock may be measured in terms of qualifications valued by the volume of expenditure on education services, but it can also be represented as the product of labour input in the economy and the average volume of human capital tied up in this labour input. To create a forecast for this representation of the human capital stock, separate projections were made of the labour input growth rate and the volume of education expenditure used in 2020–2070 for the post-comprehensive school qualifications gained by people of working age.It was the same method as used to estimate the growth rate for human capital with statistical data in the period 2000–2019.

Predictions of the size of cohorts amongst those aged between 16 and 74 for the period 2020–2070 were obtained from the population forecast made by Statistics Finland in 2021. The estimates for the annual number of students in any cohort at each qualification level were based on the assumption that in each age group the share of students starting a course to gain a qualification and those continuing one would remain the same as in the previous three to five years. On the basis of numbers of students, it was possible to predict the numbers of qualifications gained, always supposing that the share of students gaining a qualification would remain the same as in the recent past. Finally, qualifications were given a value by multiplying the number of qualifications at each educational level by the average education expenditure volume per qualification. In the no-policy-change (low growth) scenario, the assumption was that the average education expenditure volume per student would remain the same at each educational level throughout the forecast period as in 2019.

In the model, labour input is measured in terms of hours worked. The trend in number of hours worked in the years covered in the forecast depends on the increase in the number of people of working age (15–74), the labour force participation rate, the unemployment rate and the number of hours worked per employee. The working-age population of Finland will fall sharply as the population ages. The population forecast made by Statistics Finland in 2021 suggests that by 2040 there will be a good 170,000 fewer people of working age in the country than in 2020. By the end of the forecast period, i.e. 2070, the figure will be down by 480,000.

The volume of human capital in Finland has been increasing since the end of the 19th century. The trend has benefited in particular from the continuous improvement in the average educational level of the working-age population, since the new generations entering the labour market have been better educated than those retiring. Furthermore, the number of people of working age in whom knowledge and skills are embodied was increasing until around the start of the 2020s. Although the number of those of working age (16–74) began to fall in 2021, the improved average standard of education among the population will drive the growth in human capital for the foreseeable future.

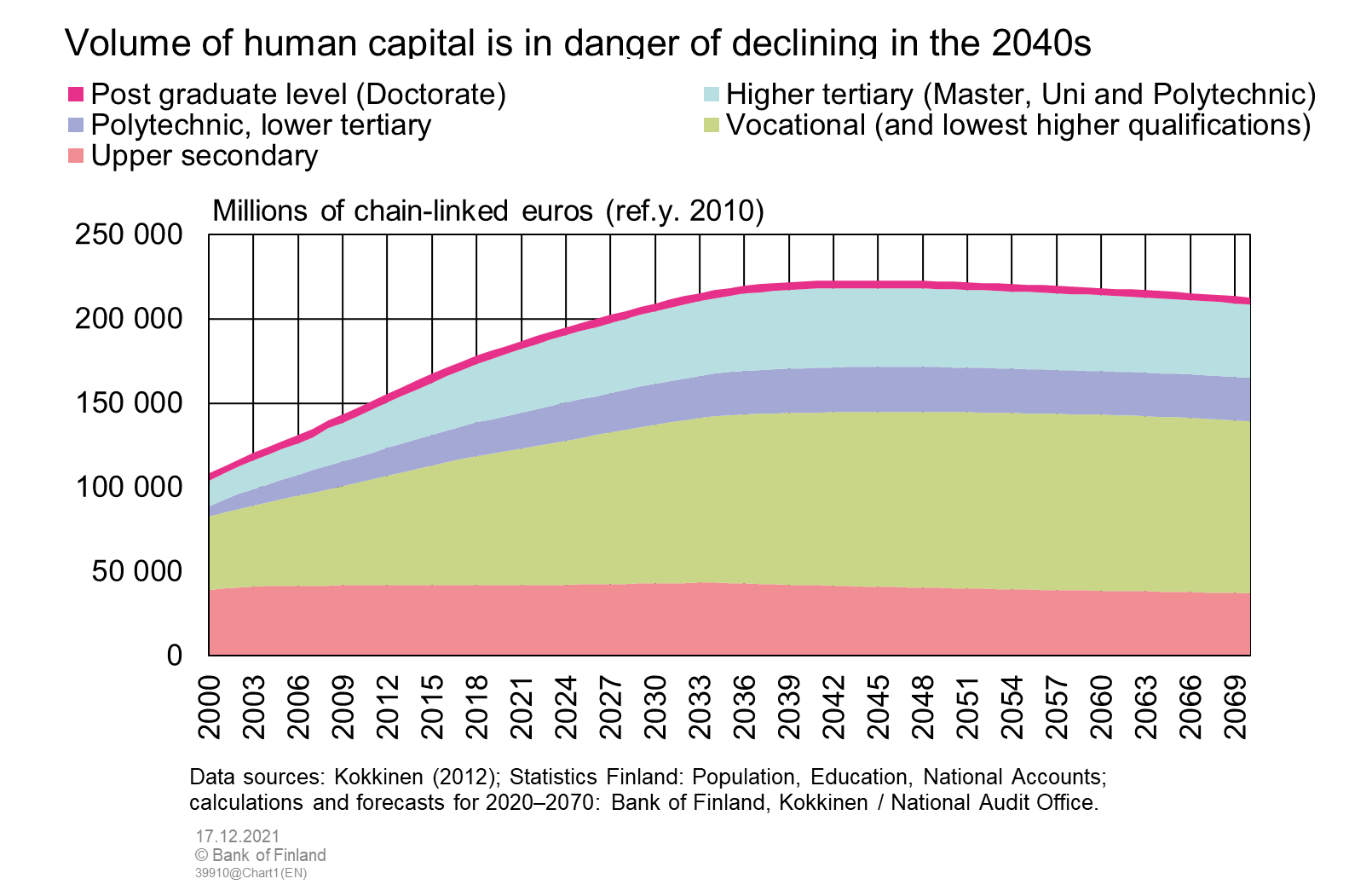

The improvement in levels of education is, however, at risk of coming to an end in the decades to come. The new age cohorts entering the labour market are still on average better educated than those retiring, but the average level of education of the youngest groups has begun to fall. The best educated cohorts are currently to be found among those born at the turn of the 1980s. At the same time, there are fewer people with university degrees, while the number of those with vocational qualifications has risen. Chart 2 depicts the trend in human capital in a situation where the decline in the working-age population continues as reflected in the latest population forecast and the educational level of the young age groups does not start to increase at the same time as the young age groups continue to become smaller in size. Human capital in this scenario still grows during the 2030s but starts to decline towards the 2050s, and that fall continues until the end of the forecast period by an average rate of 0.2–0.3% annually.

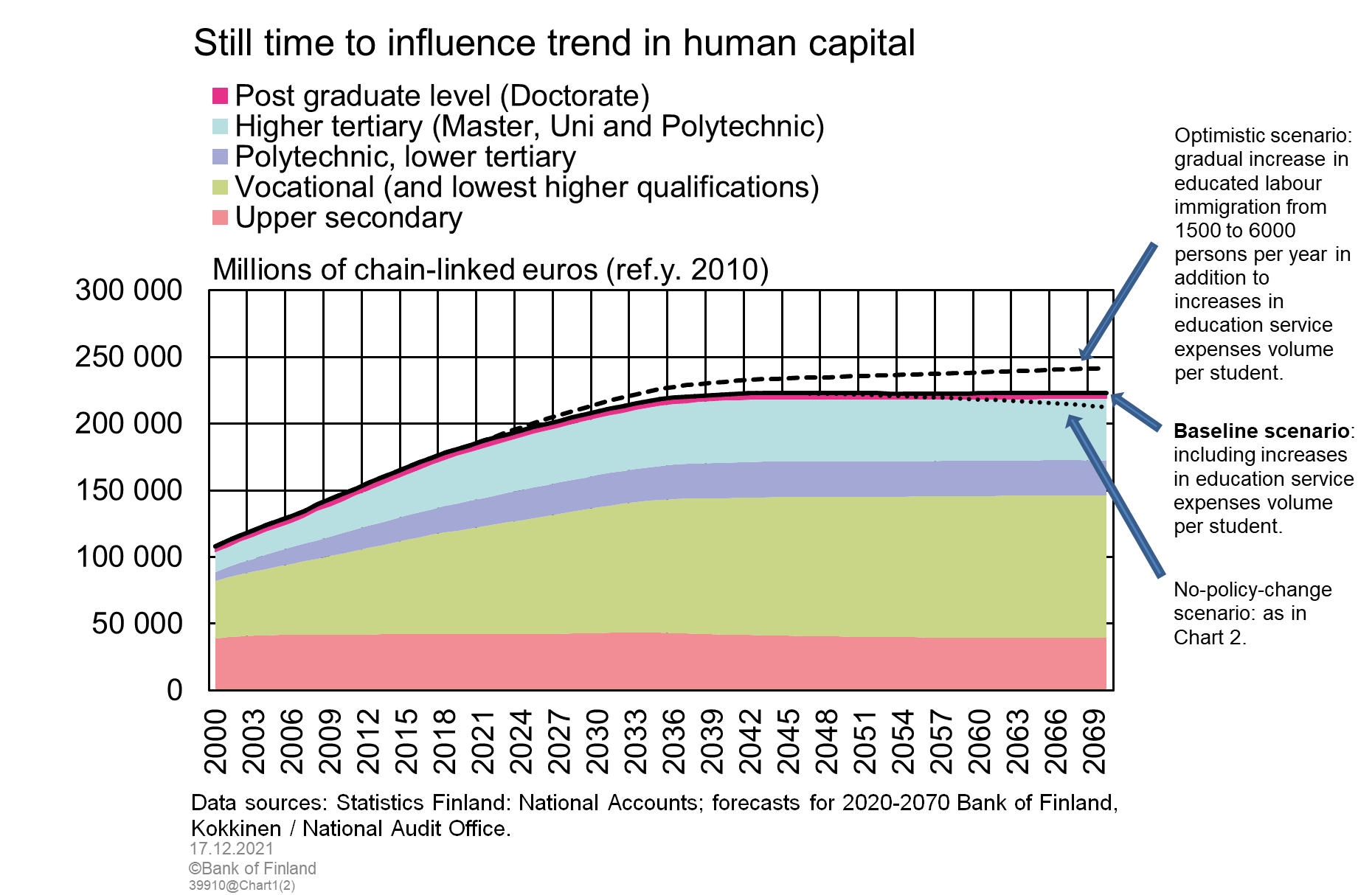

The projection for human capital growth depicted above is based on the assumption that there is no attempt actively to curb the decline in human capital by means of economic policy measures. In addition to the no-policy-change scenario, the long-term growth forecast examines two alternative, more optimistic scenarios, where an attempt is made to stop this decline. In the baseline scenario for the forecast (the middle curve), the education expenditure volumes per student are increased in the 2050s and 2060s to correspond to their level at the turn of the 1990s. In this scenario, the growth in the volume of human capital would slow significantly towards the 2040s and stop completely in the 2050s. In the third, optimistic scenario, employment-related immigration is gradually increased so that in the period 2050–2070 there would be 6,000 more immigrants per annum than now.These migrants are assumed to be as well educated as Finns who gained their qualifications in 2019. It is to be supposed that the children of migrants will join the labour force when they have gained a qualification. If these more optimistic assumptions are made, human capital would grow until the end of the forecast period, although the pace of growth would slow considerably in the 2040s.

Slow growth in fixed capital

The long-term trend in the fixed capital stock is closely linked to the growth in human capital, since the adoption of new means of production and technologies and their spread mean that the labour force needs to be able to learn new skills.Fixed and human capital in the forecast model can be substituted for each other, but the research literature on endogenous growth suggests that human capital is vital for the adoption of innovations and new technology. The relevance of learning skills is heightened as more and more investment is made in R&D rather than machinery and equipment. The ability of the labour force to innovate in R&D and embrace new technology is still to a significant extent reliant on traditional forms of education that lead to the gaining of qualifications.

The normal assumption made in theoretical growth models is that fixed and human capital should in the long-term increase at the same rate. From an historical perspective, however, economic growth in Finland does not fully support this conclusion. Both the fixed and the human capital stock grew in Finland at roughly the same rate from the 1930s until the start of the 1990s. Following the recession in the 1990s, however, the growth rate for fixed investment slowed dramatically, and since then the growth rate of the capital stock as a whole has been more dependent on the increase in human capital. The current growth forecast for the economy examines three different scenarios for how the trend in the volume of fixed capital compares with that for human capital over the period covered in the forecast, i.e. 2020–2070.

For the purposes of the growth forecast, human and fixed capital volumes in the scenarios and labour inputs had to be divided again and allocated among the three parts of the economy. The growth rate for human capital was assumed to be the same in each of these three. The assumption may be regarded as legitimate, as there is no discernible difference of any substance in Finland in the average educational level of the labour force in private as opposed to public production. The trend in volumes of fixed capital is predicted to progress in line with that for human capital in any of the three parts of the economy. In the no-policy-change scenario, the ratio of fixed capital to human capital (the K/H ratio) is consistent with the last year for which we have statistics. In the more positive baseline scenario it is assumed that this relationship will return to the level identified previously. In the highest growth scenario, fixed capital is assumed to grow in the forecast period at the same pace as the average for 1976–2019.

In the model, labour input is allocated in such a way that the need for labour in public production is determined exogenously on the basis of demand for public and publicly funded social welfare and health care services and the productivity trend in public service production. With an ageing population, demand for these services is expected to increase substantially, especially over the next two decades. Because labour productivity growth in public services has tended to be slow in the past and the rate of productivity growth is not expected to improve quickly, the need for labour in age-related services will be closely tied to the rate at which age-related expenditure increases, and will grow by around 0.4–0.5% per annum in the period 2020–2070. The rest of the labour input is in private production, i.e. manufacturing and private non-manufacturing, and is distributed between these in proportion to the respective numbers employed.

Three scenarios for economic growth in Finland

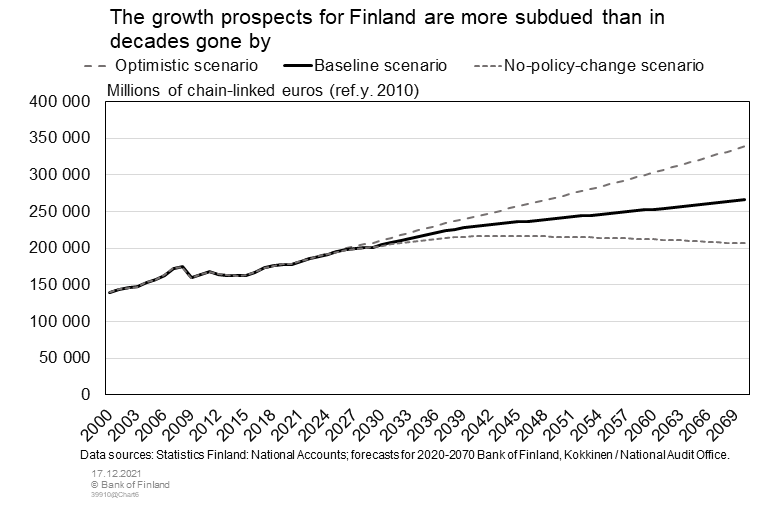

The growth prospects for Finland for the next few decades are still weaker than they seemed from the previous long-term forecasts made by the Bank of Finland. The forecast in 2018 was that the Finnish economy would grow by an average of 1.5% per annum in the period 2026–2040. The three new forecast scenarios for the country's economic growth over the period 2020–2070 are based on three separate assumptions with respect to the trends in human and fixed capital in the future (Chart 4, Table 1).

The assumption made in the baseline scenario is that it is possible to predict a slowdown in economic growth and respond to it by means of economic policy measures. Efforts are made to slow the deterioration of human capital with an increase in education expenditure volume per student from the present level to the levels seen at the turn of the 1990s.Education expenditure volume per student is assumed to remain at the same level as now in the period 2020–2040 (7,000 per annum in reference year 2010 chain-linked euros), but in the period 2040–2060 would rise to 8,200 in chain-linked euros (reference year 2010). It is also possible to increase investment in fixed capital compared with recent years, returning the K/H ratio to the level seen at the turn of the 1990s, after which it gradually declined.

Economic growth according to the baseline scenario is rather slower in the near future than the Bank of Finland predicted in its previous long-term forecast. In the 2020s and 2030s, GDP grows by an average of 1.2% per annum. From the 2040s, however, economic growth slows to 0.5% per annum, as productivity growth from the 2050s is driven only by the growth in fixed capital.

A measure of the trend in the standard of living that is even more significant than GDP is the growth in GDP per capita. In Finland, that has historically increased at the same rate as labour productivity. In the results presented in Table 1, economic growth per capita is thus also estimated on the basis of GDP per hours worked. In the 2020s, it increases by a few tenths of a percentage point more slowly than GDP, as the volume of labour input continues to rise owing to improved participation on the labour market. As the volume of labour input starts to diminish towards the 2030s, economic growth becomes more dependent on productivity than ever, with economic growth estimated per person being driven faster than the growth in GDP.

The pessimistic no-policy-change scenario is based on the supposition that the growth in (human and fixed) capital does not in any way benefit from economic policy measures. With regard to investment in fixed capital, the assumption is that the relationship between the volume of fixed capital and human capital remains much the same as it is now. It is thought that both human and fixed capital will in such a case decline by between 0.2% and 0.3% on average in the 2050s.

According to this gloomy scenario, GDP would still grow at a rate of 1.2% in the 2020s, though by the 2030s the growth rate would dip to 0.6%. Eventually, there would be negative economic growth, with the human capital stock starting to shrink and the GDP growth rate standing at -0.2% to -0.3% per annum on average in the 2050s and 2060s.

In the optimistic scenario, as with the baseline scenario, the assumption is that education expenditure volume per student is increased. In addition, the rate of growth of human capital is supported by an increase in work-related immigration from the 2030s compared with the current figure of around 1,500 persons per annum. Immigration is assumed to increase gradually, reaching a figure of 6,000 persons per annum in the period 2050–2070.

The assumption is also made that fixed capital grows steadily from the 2030s at the same annual rate of 2% as was seen on average during the period 1976–2019. The volume of fixed capital in relation to human capital in this case eventually becomes larger than in the baseline scenario.

The faster rate of growth of both fixed and human capital would speed up productivity growth compared with the baseline scenario, with GDP in the 2020s and 2030s increasing at a rate of around 1.5% per annum, i.e. about as fast as in the Bank of Finland's previous long-term forecast. Economic growth towards the 2040s would nevertheless wane in this scenario, too, falling to an annual rate of 1%.

Table 1.

| Three scenarios for economic growth in Finland in the period 2010–2070, growth rate of variables (%) | ||||||||||

| No-policy-change, low growth scenario | Y/L resid | K/L | L | H/L | Y/L | Y resid | H | K | Y | |

| 2010–2019 | -0.6% | 0.8% | 0.4% | 2.0% | 0.8% | -0.6% | 2.3% | 1.2% | 1.1% | |

| 2020–2029 | -0.1% | 1.2% | 0.1% | 1.2% | 1.1% | -0.1% | 1.3% | 1.3% | 1.2% | |

| 2030–2039 | 0.0% | 0.7% | -0.1% | 0.7% | 0.7% | 0.0% | 0.6% | 0.6% | 0.6% | |

| 2040–2049 | 0.0% | 0.3% | -0.3% | 0.4% | 0.3% | 0.0% | 0.0% | 0.0% | 0.0% | |

| 2050–2059 | 0.0% | 0.4% | -0.5% | 0.4% | 0.4% | 0.0% | -0.2% | -0.2% | -0.2% | |

| 2060–2070 | 0.0% | 0.3% | -0.5% | 0.3% | 0.3% | 0.0% | -0.3% | -0.3% | -0.3% | |

| Baseline, middle growth scenario | Y/L resid | K/L | L | H/L | Y/L | Y resid | H | K | Y | |

| 2010–2019 | -0.6% | 0.8% | 0.4% | 2.0% | 0.8% | -0.6% | 2.3% | 1.2% | 1.1% | |

| 2020–2029 | -0.1% | 1.2% | 0.1% | 1.2% | 1.1% | -0.1% | 1.3% | 1.3% | 1.2% | |

| 2030–2039 | 0.0% | 1.8% | -0.1% | 0.7% | 1.3% | 0.0% | 0.6% | 1.7% | 1.2% | |

| 2040–2049 | 0.0% | 1.3% | -0.3% | 0.4% | 0.8% | 0.0% | 0.1% | 0.9% | 0.5% | |

| 2050–2059 | 0.0% | 1.4% | -0.5% | 0.5% | 1.0% | 0.0% | 0.0% | 0.9% | 0.5% | |

| 2060–2070 | 0.0 % | 1.4% | -0.5% | 0.5% | 1.0% | 0.0% | 0.0% | 0.9% | 0.5% | |

| Optimistic, high growth scenario | Y/L resid | K/L | L | H/L | Y/L | Y resid | H | K | Y | |

| 2010–2019 | -0.6% | 0.8% | 0.4% | 2.0% | 0.8% | -0.6% | 2.3% | 1.2% | 1.1% | |

| 2020–2029 | -0.1% | 1.5% | 0.1% | 1.4% | 1.4% | -0.1% | 1.6% | 1.6% | 1.5% | |

| 2030–2039 | 0.0% | 2.0% | 0.0% | 0.8% | 1.4% | 0.0% | 0.8% | 2.0% | 1.4% | |

| 2040–2049 | 0.0% | 2.2% | -0.2% | 0.4% | 1.4% | 0.0% | 0.2% | 2.0% | 1.1% | |

| 2050–2059 | 0.0% | 2.3% | -0.3% | 0.4% | 1.4% | 0.0% | 0.1% | 2.0% | 1.1% | |

| 2060–2070 | 0.0% | 2.3% | -0.3% | 0.4% | 1.4% | 0.0% | 0.1% | 2.0% | 1.1% | |

| Y = gross domestic product; L = labour; K = capital; H = human capital | ||||||||||

Growth in private production relies on productivity growth

The growing demand for age-related services owing to an ageing population was taken into account by dividing the economy in the forecasting model into public production, manufacturing and private non-manufacturing. Employment in public production will depend directly on demand, and the rest of the labour input will be distributed within private production. The three parts of the economy will grow at virtually the same rate throughout the forecast period, but a very evident difference in the composition of growth will emerge between them, particularly after the 2030s. Labour input in public production, which is determined on the basis of the demand for public services, will still increase even after the 2030s, with the demand for social welfare and health care services continuing to rise. The labour input not in public service production will be distributed among private production, and after labour input declines, growth in private production will have to rely on productivity growth alone.

Conclusions and discussion

Although the COVID crisis does not appear to be leaving permanent scars on the Finnish economy, the long-term growth prospects remain subdued. With the ageing population, the size of the labour force will eventually decline, and there are no signs of any acceleration in labour productivity growth either. According to the baseline scenario in the forecast, economic growth in the next couple of decades will remain at 1.2% and weaken from the 2040s onwards.

In the Bank of Finland's new long-term forecasting framework, economic growth will depend on the rate of growth of both fixed and human capital. As the educational level of those of working age has continuously improved, economic growth in Finland has been kept going mainly by the accrual of human capital. The importance of human capital was especially evident following the years of recession in the 1990s, when investment in fixed capital was limited. However, the volume of human capital in Finland is in danger of declining in the 2040s if the current downward trends in population growth and education are not reversed: the young age cohorts entering the labour market are constantly growing smaller, in addition to which those born at the start of the 1980s are, at least so far, the best educated age group ever in Finland.

It is possible to slow the deterioration of human capital with additional investment in education and more robust incentives for acquiring skills, participating in the labour force and increasing the birth rate. Furthermore, it is possible to increase immigration of skilled workers, which would be more readily reflected in the volume of human capital than merely relying on policy measures that relate to the indigenous workforce alone.

Labour productivity growth depends not only on the trend in human capital but also on investment in fixed capital. Innovation spreads in business mainly through the deployment of new and better machinery, equipment and software and the adoption of ideas for products conceived in R&D. Technological development therefore also in practice relies on both investment in fixed capital and in R&D. The forecasting model used here does not include a detailed description of fixed capital accumulation, and the trend in the fixed capital stock in relation to human capital is based on simplified assumptions. The accumulation of fixed capital is therefore surrounded by the same uncertainty as that pertaining to the assumptions concerning the rate of growth for total factor productivity in neoclassical growth models. The main conclusion about the significance of fixed capital for productivity growth remains, however. Nevertheless, in a small open economy such as Finland's, it is not possible to invent and develop everything at home: in the future too, most new technology will be imported from abroad. That is why investment in fixed capital from abroad, including the outcomes of R&D, cannot be ignored.

The impact on annual economic growth of the economic policy measures examined in the forecast would not be great, but even a small acceleration in economic growth will over the decades result in a major improvement in living standards. An increase in the working-age population would also help reduce the dependency ratio, which is threatening the sustainability of the public finances.

corliswiliturkered.blogspot.com

Source: https://www.bofbulletin.fi/en/2021/5/finland-s-new-long-term-forecast-suggests-gdp-growth-will-be-more-subdued/